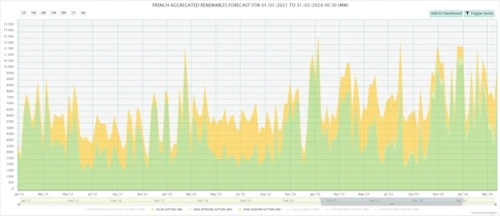

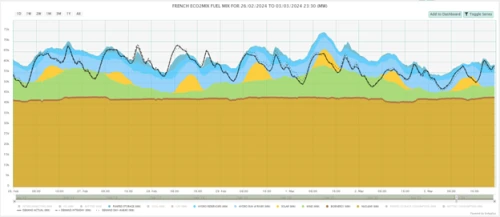

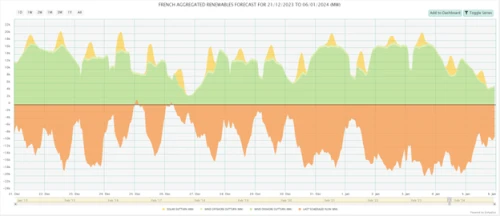

French fuel mix: zero carbon and below zero prices

Ahead of French Energy day 2024, Market Expert and Territory manager for France, Clement Bouilloux takes a look at the changing French fuel mix, explaining why the country's unique mix of nuclear and renewable generation is placing downward pressure on power prices.

Looking for more insights into energy markets?