Guarantees of Origin: market trends 2024

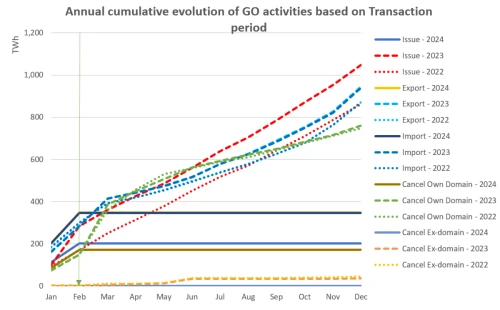

2023 was another exceptional year for Guarantees of Origin. A large price spread between in-year and future vintages, notable changes to regulation and significant price volatility all played their part in changing the face of the market. In this blog post, Market Expert, Laura Malinen outlines the key topics impacting GO markets in 2024.

Read our Guarantees of Origin trends 2025

EU European Electricity Market Summary

Our expert analysis of key trends, challenges, and milestones shaping Europe’s electricity market in 2024

Looking for GO price benchmarks?